Catch a Falling Star: Good Targets in the Chinese Privatization Trend

Recently we have seen an avalanche of US listed Chinese companies deciding to take themselves private. The primary reason is the current share price severely undervalues these companies compared to their book or net asset values. This is the direct result of short attacks that have taken advantage of the few cases of fraud and misrepresentation existing in this sector. Those black sheep have enabled short interest to easily smear reputable Chinese companies by pointing out the slightest real or as is mostly the case, perceived discrepancies in their financials.

It should be obvious to all that the companies who have taken themselves private and those who are just entering the process are not frauds. Why would anyone want to buy a house of cards of their own making with their own money? All of them however were the targets of attacks by shorts.

A very good article on these events appeared here on Seeking Alpha and if you are interested in this topic you should also read: An Epic Saga Comes to an End. This article makes several good points including the following one. “…. not all (Chinese stocks) are fraudulent and at some point the risk/reward will shift to the other side, as the entire space is currently mispriced relative to fundamentals due to the overwhelming short interest”.

To demonstrate the strength of this trend consider the following list of companies that have: 1) gone back to China (privatized) or 2) are in the process or are likely privatization candidates.

1) Taken Private or Announced Plans

Andatee China Marine Fuel Services Corporation (AMCF)

Chemspec International Ltd. (CPC)

China Advanced Construction Materials Group, Inc. (CADC)

China Fire Security Inc. (CFSG)

China GrenTech Corporation Limited (GRRF)

Fushi Copperweld Inc. (FSIN)

Global Education Technology G (GEDU)

Harbin Electric Inc. (HRBN)

Shanda Interactive Entertainmen (SNDA)

SOKO Fitness Spa Group, Inc. (SOKF)

2) Candidates for Announcements

Advanced Battery Technologies, Inc. (ABAT)

American Lorain (ALN)

China Auto Logistics (CALI)

China Shengda Packaging Group (CPGI)

China XD Plastics (CXDC)

ChinaCast Education Corporation (CAST)

Lihua International (LIWA)

Telestone Technologies Corp. (TSTC)

Winner Medical Group (WWIN)

The following sampling of news items, over just the last few days covering these recent events show the breath and magnitude of this changing dynamic in the US listed Chinese stocks. They also provide credence to the prospect that going or staying short in these stocks is fast becoming a very risky prospect.

Wall Street Journal, Nov 23, Take-Privates Capture Asian Bankers’ Fancy Battered Chinese companies listed in the U.S. or Singapore could be a feast for MA bankers who see opportunities for take-private deals. In an interview with Dow Jones Newswires, Citigroup MA banker Colin Banfield says this will be an increasingly important revenue source for bankers in the region.

Market Watch, Nov 22, Citigroup taking U.S.-listed Chinese firms private “We have several take-private deals in the pipeline,” said Colin Banfield, Citigroup’s head of mergers acquisitions, Asia Pacific…”

Business Wire, Nov 22, 2011, Goodwin Procter Dec. 8 NYC Event to Focus on Going Private and Re-Listings of Chinese An expert panel discussion will take place in New York City at Goodwin’s offices on December 8 at 4:00 pm. The event will focus on issues related to the recent trend of Chinese companies going private in the United States and seeking re-listing in China.

Business Wire, Nov 21, 2011, U.S. Capital Market: Survive, Go Private and Beyond” at the 2011 Halter Financial Summit With all the negativity centered around U.S.-listed Chinese companies, many companies are reevaluating the high listing costs, regulatory burdens and increased SEC scrutiny associated with being a U.S. Public company. For companies no longer interested in remaining listed in the United States, they have the option to terminate their U.S. Listing by going private.

Reuters, Nov. 15, U.S.-listed China firms welcome to come home Zhou Qinye, the exchange’s vice general manager, said while only a few firms have real accounting issues, many overseas investors are short-selling Chinese companies for profit.

Capital Markets, Nov. 2011, GOING PRIVATE The honeymoon over, many mainland corporations listed in the United States are scrambling for the haven of private ownership Private equity firms have spotted the low valuations of these troubled companies and started pursuing majority shareholding with a view of snapping them up for a song. “Many industry participants have noticed that the trading multiples of such U.S.-listed Chinese businesses are often lower than those of comparable companies listed on the Hong Kong stock exchange,” notes Doug Warner, a partner at the Weil, Gotshal Manges law firm in New York.

REUTERS: Business Law Currents, Nov. 8, Unfavorable investor sentiment and a downturned market in the United States have sparked a wave of management-led buyouts at U.S.-listed Chinese companies.

Two Chinese companies have announced privatization in the last few days.

PR Newswire, Nov. 23, China Marine Fuel Confirms Receipt of Notice from Majority Shareholder and Chief Executive Officer Andatee China Marine Fuel Services Corporation (NASDAQ: AMCF – News) (“Andatee”), a leading producer, distributor, and retailer of quality marine fuel for small cargo and fishing vessels in China , today confirmed that it has received notice from An Fengbin of his intention to launch a tender offer to acquire all of the outstanding shares of Andatee that he does not already own.

PR Newswire, Nov. 21, 2011, Special Committee of Fushi Copperweld, Inc. Announces Receipt of Revised ‘Going Private’ Proposal at $9.25 Per Share The Special Committee of the Board of Directors of Fushi Copperweld, Inc. (“Fushi” or the “Company”) (Nasdaq: FSIN) today announced that it has received a revised proposal from its Chairman and Co-Chief Executive Officer, Mr. Li Fu and Abax Global Capital (Hong Kong) Limited on behalf of funds managed by it and its affiliates (“Abax”), for Mr. Fu and Abax to acquire all of the outstanding shares of Common Stock of Fushi not currently owned by Mr. Fu and his affiliates in a going private transaction for $9.25 per share in cash, subject to certain conditions.

This surge in US listed Chinese companies going private presents us with two great opportunities, finding companies on the cusp of going private, but which have not yet announced and ferreting out legitimate companies that have suppressed share prices because of short attacks. The later category consists of companies that are working hard to establish their trustworthiness by being transparent and allowing the kind of scrutiny that will guarantee a positive change in credibility and sentiment. One company, Lihua International (LIWA), seems to meet both of these criteria.

Fushi Copperweld Inc. (FSIN) is important to our discussion here because it is a very similar company to Lihua International producing copper-clad bimetallic engineered conductor products for electrical, telecommunications, transportation, utilities and industrial applications. If this sounds familiar it should, as it is an almost identical description of Lihua’s business and products that were described in this SA article.

Lihua International like many of the companies that have already announced they are going private has been engaged in a long and protracted process of trying to shed the short stigma by adopting a policy of complete openness and full disclosure.

There has also been a long and in all probability, not coincidental string of statements that when taken into the context of the recent announcements detailed above, makes it seem evident that LIWA is joining the fray of companies going private.

In preparing for a recent Seeking Alpha article on LIWA I had the opportunity to ask the CFO several questions regarding its financials. I followed up this conversation with a question I had raised in my previous article. Was LIWA’s management going to take the company private? Her response was not “no.” It was “I can not comment or respond to that question!” There is only one reason that this response was anything other than a simple no. Management legally cannot disclose a material decision to a reporter that this option is being undertaken or is even under consideration. Otherwise it seems obvious that a simple, polite “no” would have been the immediate, appropriate and reflexive response.

She did allow that several private equity firms specializing in just this type of privatization have approached the company. “In this market it is quite common for companies like LIWA to be approached unilaterally with offers of these types of services” Ms. Huang stated.

But it gets more intriguing as you continue to look closer.

During the question and answer section of Lihua’s third quarter 10Q financial conference call, the CFO was asked the following question by Michael Scholten, CFA Investment Manager of CLEAR HARBOR ASSET MANAGEMENT, LLC., Clear Harbor currently holds 675,479 shares of LIWA.

Clear Harbor: “Could you provide us with an update on the buyback?”

Lihua CFO: “Sure Mike, right now we are within the quite period and we are expecting to be in a quiet period in the next few months. So currently we are holding the share buy back.”

Clear Harbor: “Ok, you are in a quiet period for the next few months? Even though you have just reported your earnings?”

Lihua CFO: “Um, laugh, the rules for insider trading restriction, um, part of that is close to the financial quarter end, um, but there is also, um, a limitation of, those in possession, such as items of insiders, in possession of material non public information.”

There are three very unusual and interesting questions raised by this exchange. The first is the quiet period for the company ends 48 hours after the release of their financials. That would normally end Lihua’s quiet period on Nov. 11, 2011. The response to Michael Scholten’s question can only have one interpretation. There are additional and as yet undisclosed “Material non public Information,” issue(s) that are currently ongoing within Lihua. When you couple the cessation of the share buyback program this takes on added meaning. Companies in possession of non-public material information are prohibited from purchasing shares in the open market. One other important element exists here and that is a requirement to immediately release material information that is negative or has the potential to have a negative impact on the companies financials or its share price as soon as it becomes apparent or know to the company. The company is not releasing this information and indeed may not do so within “the next few months.” The only reasonable conclusion that can be drawn from these exchanges is there is good news coming from Lihua shortly, but we cannot conclusively state that it’s a privatization move on the company’s part. Although the line of dominoes would certainly lead any reasonable person to that conclusion. Any kind of merger, reverse merger or acquisition would also mandate this same type of quiet period.

As the following press release, dated Oct 24, 2011 indicates, a strategic shuffling of Lihua’s management occurred recently. Lihua International Appoints Daphne Huang as Chief Financial Officer Ms. Huang is a Chinese American who understands how Wall Street works and will be more effective at negotiating on Lihua’s behalf. The following career highlights make it clear that she is an ideal candidate to lead the team taking this company private and this could well be the primary reason that their long time CFO, Mr. Yang “Roy” Yu, was moved from this position and appointed as the Company’s Executive Vice President of Finance. Ms. Huang previously served as Lihua’s Executive Vice President of Corporate Finance and Director of Investor Relations since October 2009. Reading Ms. Huang’s resume will immediately tell you why the company would want this rich resource of talent and experience at the helm of a privatization action.

Prior to joining Lihua, Ms. Huang served as a Vice President in the Debt Capital Markets group at GE Capital Markets, Inc. from 2003 to 2009, where she played an important role in structuring, underwriting and syndicating some $2.5 billion of debt products. From 2000 to 2002, she was a Senior Associate in the Debt Capital Markets group at Fleet Securities, Inc., which was later acquired by Bank of America. From 1997 to 2000, Ms. Huang was a Senior Auditor in the Capital Markets Group at Price Waterhouse Coopers LLP, and from 1996-1997, she was an equity research analyst at Cowen Co. She began her career as a mutual fund analyst at Morgan Stanley Dean Witter. Ms. Huang received an MBA in Finance and Management from the Leonard N. Stern School of Business at New York University, a BBA in Accounting from Baruch College, and holds an inactive CPA license in the state of New York.

This seems to be a sentiment held by their CEO “Since joining Lihua after the listing of our common stock on NASDAQ, Daphne has made substantial contributions to our strategic direction and has served as the face of our Company to the investment community.”

Why would Lihua want to go private?

Lihua International has a perception problem. It looks too good to be true. The reason for this misconception is easily explained. Lihua is a commodity-based company. It utilizes copper in the production of its products, which have been detailed in a previous SA article here.

As the cost of this commodity increases, the cost of Lihua’s finished goods increase at the same rate. Copper prices have risen from $3,000 dollars a ton in 2008 to $11,500 in Feb. of 2011. This is a 275% increase in the cost of goods and has made Lihua’s revenue go up at this same soaring rate. Lihua’s revenue increases would look similar if its underlying commodity was gold. Gold in the same time frame went from $600 dollars an ounce to $1,800 and ounce at it’s high this year. That is a 200% increase in price. There are no jewelry stores in the country that have not seen soaring revenues while at the same time experiencing flat or declining profits. Of course all of these jewelry stores pass along the increased cost of good in the manufacturing process to their wholesales and end users, but none of them are being accused of fraudulent business practices.

LIWA’s copper costs are passed along to its clients as well just as all cost by all profitable businesses are. The gross revenue (actual profit derived from the value it added during manufacturing and processing minus operating cost) is completely in line with industry norms.

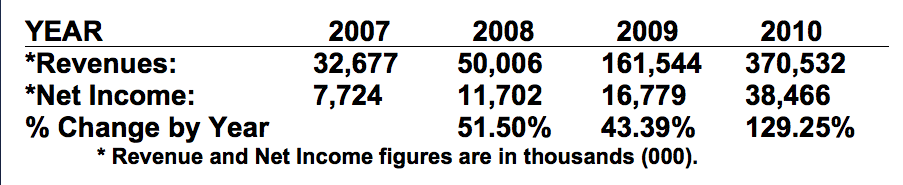

Here are the Revenues and Net Income by year of Lihua.

{kind=link}

Keep in mind that between 2008 and 2010 the price of a ton of copper increased 233%. Lihua’s production and demand have also increased during this same time frame.

Short interest has pummeled this company by pointing out that there is no way a company could sustain this type of increased revenue, year over year, and still be legitimate. They of course always omit the reason for these soaring revenues. The finished price of its products has soared as the underlying costs of the copper utilized to produce them have also dramatically risen. This simple straightforward truth would obviously undermine their purpose of deceiving enough investors to drive the price down.

So let’s look at its profits as compared to industry peers.

Encore Wire Corporation (WIRE) gross margins have fluctuated between about 8% and as high as almost 20% historically. In the most recent quarter, WIRE’s gross margin was 11.8% and averaged ~11% during 9 months of 2011. LIWA’s gross margins were 12.5% in Q3of 2011 and averaged at about 12% during 9 months of 2011. LIWA’s gross margins are perfectly in line with Chinese and US competitors when you consider that LIWA uses cheaper scrap copper verses WIRE’s virgin copper as well as the fact that LIWA also sells Copper Clad Aluminum wire with much higher margins compared to copper wire.

Looking at operating margins, LIWA’s is about 11% for the last 9 months while WIRE’s is about 5.5%. First of all, WIRE is located in the US so it would have substantially higher labor and overhead expenses. The US has more demanding environmental or OSHA regulations further driving up the cost of doing business here. WIRE has a much larger facility, capacity and asset base compared to LIWA, so its depreciation is higher.

Lihua’s cost is less because its base material supplies are obtained from scrap copper. Its products can go into many different industries and a wide variety of products, meaning that a lot of the demand for their products naturally comes to LIWA. This eliminates the need to spend a lot on advertising, sales or transportation expenses making its products less expensive and more competitive. All of this explains why LIWA’s operating margins are higher compared to WIRE’s while its gross margins are very similar.

Fushi Copperweld, Inc. (FSIN) as another example. FSIN’s operating margins are much higher than LIWA’s and stand at about 18%. Does this mean that FSIN is a fraud and LIWA is real just because FSIN has higher margins? No, each one of these companies has its own specifics in supply, demand, distribution, and manufacturing. As noted above Fushi Copperweld has just announced that it is going private at $9.50 a share. It’s not a fraud!

The only other issue that could and has been lodged against Lihua by short interest, is it does not possess the required assets to produce the profits it is posting. The asset argument is dumb, without any merit and is designed simply to scare people. Many responsible and creditable individuals have visited LIWA’s facility and saw that the production assets exist and where in use. There are lots of posted photographs of LIWA’s infrastructural resources that can be viewed here, here and in any of its many industry and investor presentation pdf’s that can be found here.

Multiple parties verified LIWA’s total capacity, so we know that LIWA can sell as much as it is claiming using those assets. LIWA’s scrap copper purchases and copper sales (as well as customer checks) were reconciled by an independent report produced by China 360, along with its domestic filings, which have been demonstrated that they matched SEC filings. In addition, its cash levels were verified and daily cash activity compared with invoices from customers to suppliers by John Lees Associates.

If Lihua decides to go private it will be to escape the depressed share price that negative, misleading and deceptive short attacks have caused. Currently their price-per-share is $5.33 and that represents less than half of its current book or net asset valuation. As any publicly traded company will tell you, an artificially suppressed market cap dramatically interferes and impedes with its ability to make forward looking decisions that are in the best interest of the company’s investors.

Lihua is a healthy company with $102 million is cash and cash equivalents in verified accounts. Lihua is now expanding the company’s manufacturing capacity using free cash flow generated from profits. LIWA is a sound and easily verifiable long-term investment that may not be a publicly traded company in the very near future. If the company is taken private or acquired by a competitor look for a significant premium over the recent trading range.

I was quite unhappy with the deceptive short interest in LIWA shares, but as it turns out they may be doing long-term and new investors a service by providing a great entry point to a very profitable privatization trade.

Disclosure: I am long LIWA.

Additional disclosure: I hold no positions in any other company mentioned in this article and have no intention in initiating positions in the next month.